Eurozone Crisis and Banks' Creditworthiness: What is New for Credit Default Swap Spread Determinants? - Alessandra Ortolano, Eliana Angelini, 2022

Descrição

Risks, Free Full-Text

Histogram of network heterogeneity measure

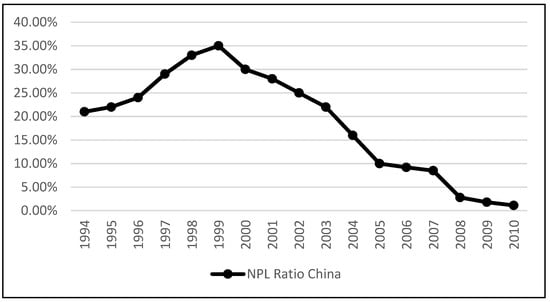

Percentages of banks' non-performing loans to total gross loans. Grey

Alessandra ORTOLANO, Research Assistant, Tuscia University, Viterbo, Tuscia, Department of Economics, Engineering, Society and Business Organization - DEIM

VaR performance in the real economic and subprime crisis

PDF) The Impact of the Sovereign Debt Crisis on Bank Lending Rates in the Euro Area

Eliana ANGELINI, Università degli Studi G. d'Annunzio Chieti e Pescara, Chieti, UNICH, Department of Economics

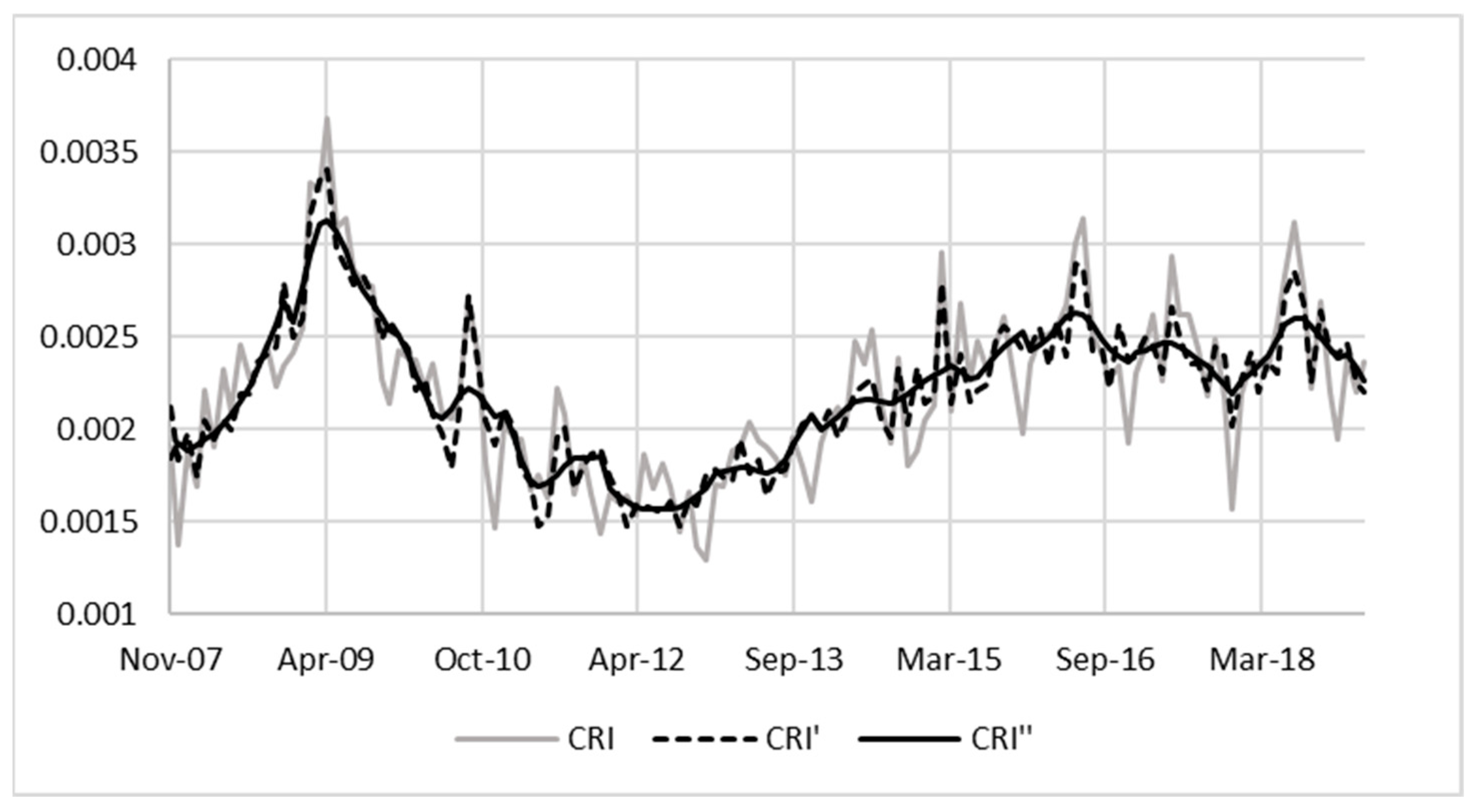

Granger casual relationship betweenˆρbetweenˆ betweenˆρ t and real economy.

Historical values of the S&P500 VIX; period 01.1990-12.2010

PDF) Fundamental determinants of credit default risk for European and American banks

Moving decomposition of the R2

Risks Special Issue : Credit Risk Management

de

por adulto (o preço varia de acordo com o tamanho do grupo)